Page Navigation

Select a different country or region to view content tailored to your location.

Chris Cammack is the Partner Manager and a financial writer at FxScouts. Chris builds and maintains our relationships with our partners to provide our users with the best Forex trading experience.

Regulation is the single most important consideration when choosing a broker. We only work with the best well-regulated Forex brokers. In this article, we discuss how regulation impacts traders and why it's so important.

Over the last two decades, the explosion of online Forex (FX) and contract for difference (CFD) trading has attracted millions of traders with its low cost of entry, high leverage, convenient mobile access, and tempting bonuses and promotions. According to the Bank for International Settlements, “trading in OTC FX markets reached $7.5 trillion per day in April 2022,” making it the largest financial market in the world. But in the 2000s, when online Forex trading was in its infancy, regulators had only just started to take an interest in how Forex brokers operated.

After the subprime mortgage crisis of 2007 and the great recession that followed, financial regulators in Europe and North America decided to more closely monitor and regulate complex financial products. While most of their focus was on mortgage-backed securities (MBOs) and collateralised debt obligations (CDOs), which lay at the heart of the crisis, online CFD trading was also included in their review.

Regulators quickly realised that many retail CFD traders, i.e. non-professional traders with little financial education, were losing more money than they could afford and that Forex and CFD brokers were engaged in various unethical practices that contributed to these losses. An important aspect of a financial regulator’s duties is consumer protection, so regulators enhanced their monitoring of Forex and CFD brokers and quickly sought to put safeguards in place to protect consumers.

These efforts to protect traders first bore fruit in 2018 when the European Securities and Markets Authority (ESMA) passed a law requiring all EU financial regulators to set restrictions on Forex and CFD trading. These included:

EU regulations already prohibited brokers from commingling client and company funds and banned non-EU-regulated brokers from advertising their services to EU residents. With the additions of the new restrictions, losses made by retail traders began to fall - along with the profits made by EU-regulated brokers.

ESMA’s restrictions on Forex and CFD trading are now seen as the gold standard of regulation worldwide, and many regulators have followed their lead - implementing some or all of the restrictions.

Following consultation feedback, in 2019, the UK’s Financial Conduct Authority confirmed that it, too, would require Forex brokers in its jurisdiction to follow the same regulations. However, it went a step further in January 2021 when it published rules banning the sale of cryptoasset CFDs to retail consumers.

Likewise, in 2021, the Australian Securities and Investment Commission (ASIC) implemented the same regulations, except for the risk warning requirement. The Securities Commission of the Bahamas (SCB) also instituted almost all the same restrictions, though it limited maximum leverage to 200:1.

Forex and CFD transactions occur over-the-counter (OTC) with no central exchange monitoring trades, unlike stock markets. This makes it very difficult for national regulators to monitor Forex brokers and protect consumers. If a Forex broker is not located in the same country as the regulator, the regulator has no authority over the broker’s products or behaviour.

As a result, brokers based in “offshore” localities (such as the British Virgin Islands, the Marshall Islands or Vanuatu) with weak, or completely absent, regulation can engage in scams, charge exorbitant fees, commingle client and company funds, expose clients to extreme leverage, and engage in other unethical practices.

For this reason, it’s not only the quality of a broker’s regulator that a trader should be aware of but also the regulator’s location.

It is usually, though not always, preferable to trade with a broker regulated by the financial authority of your country of residence. This means that if you have a dispute with your broker, you can complain to your regulator, and they will intervene - or at least pass your case on to the financial ombudsman for arbitration.

Unfortunately, some national regulators - like the Central Bank of Nigeria or the CVM in Brazil - do not regulate Forex or CFD trading at all, or they lack the power to enforce regulations. In this case, trading with a broker regulated by a good overseas regulatory authority is better. At least this way, you will be safe knowing that you will not be scammed or fall victim to unethical business practices, though you will not have local protection.

Below is a depiction of the various regulators and their jurisdictions. Regulators at the top of the triangle are the world’s top regulators, while those at the bottom provide virtually no regulatory oversight.

**Regulators of the EEA in alphabetical order:

We consider numerous factors when deciding which tier a regulator belongs to.

Rules and Regulations: These are the legal obligations regulators place on brokers and other financial services companies. For example, all regulators require brokers to segregate their operating capital from their clients’ trading funds to prevent client losses in the event of broker bankruptcy. Tier 1 regulators, like the FCA or CySEC (of Cyprus in the EU), also require brokers to limit the leverage they offer and provide all their clients with negative balance protection. Most regulators in Tier 2 and below have more relaxed leverage limits or do not require negative balance protection. Those in Tier 4 and below either have very few rules for brokers or none at all. The organisations in Tier 5 are not regulators at all, they allow any financial company to register within their jurisdiction but do not provide any oversight or management.

Enforcement: How well a regulator enforces rules and regulations is equally important. There is no point in regulators requiring brokers to treat traders fairly if they don’t follow up on complaints, conduct audits and carry out surprise on-site visits. This is where some regulators struggle. Most of the Tier 3 and 4 regulators are well-intentioned but fail to enforce their rules consistently. All Tier 1 regulators are proactive, strict and ruthless when enforcing regulations.

Consumer Protection: A central pillar for all regulators is protecting consumers. This includes education and outreach, working closely with brokers to ensure that an appropriate level of due diligence is carried out on clients, passing on valid complaints to the financial ombudsman for arbitration, and taking rule-breakers to court and removing their licences to operate.

Because one of the most important criteria for traders when choosing a Forex broker is its regulatory status and under which authority it is regulated, we have curated a list of the major regulatory bodies by country and summarise the rules applicable to Forex brokers in that region. We will start with the British regulator, the Financial Conduct Authority (FCA).

A tier-1 regulator, the UK’s Financial Conduct Authority is one of the world's best financial regulators and has a reputation for guaranteeing trader security. It has more restrictions than regulators in lower tiers and enforces its rules efficiently.

Trading with an FCA-regulated Forex broker is particularly advantageous for British traders. FCA-regulated brokers must have a physical office in the UK to ensure that British laws govern disputes. If your FCA-regulated broker goes bankrupt, you can walk into any branch of your broker’s local bank and remove all your funds from your segregated account - this is not so easy if your money is in a foreign bank account. Local bank accounts also mean bank transfers between British clients and brokers are faster and cheaper.

FCA’s Rules

All FCA-regulated brokers must segregate client funds, provide negative balance protection, process withdrawals instantaneously, and provide compensation of up to 50,000 GBP to protect traders against broker-related matters. It also restricts leverage to 30:1, bans Forex brokers from offering bonuses and promotions, and bans crypto CFD trading.

Although the leverage limits placed on retail clients may seem restrictive, this will be the same for all brokers operating in the EU or UK. To access higher leverage, a retail trader has to qualify as an Elective Professional trader (EPC). To do so, they will have to satisfy certain eligibility criteria, such as:

It’s no surprise that their search function is the easiest to use and the most thorough, you can access it here: https://register.fca.org.uk/s/.

Like other major regulators, all brokers with an FCA licence must publish their FCA reference number on their website.

Watch this video for more information on how to check if your broker is FCA-regulated:

Also a tier-1 authority, the Australian financial regulator has an excellent global reputation and closely monitors brokers to reduce fraud and manipulation. Many of the most respected Forex brokers worldwide are Australian, and having an ASIC licence automatically signifies that the broker is trustworthy.

ASIC has a reputation for guaranteeing trader security and dealing harshly with bad brokers. Still, in March 2021, ASIC deployed an even stricter regulatory environment, including restricting leverage to 30:1, banning bonuses and promotions, and ensuring that traders are granted automatic negative balance protection.

Checking a broker’s regulatory status with ASIC is similar to the UK's FCA. The ASIC search tool can be found here: https://connectonline.asic.gov.au/.

CySEC is the foremost regulator in the EU, and Cyprus has a long history of regulating online Forex brokers. As a European regulator, all brokers with a CySEC licence must abide by the EU’s MiFID II legislation. Among other things, this requires limits on leverage, automatic negative balance protection, and a ban on trading bonuses.

CySEC’s broker search tool functions much like the FCA’s, and all CySEC licenced brokers must publish their licence number on their website. CySEC’s database and search tool can be found here: https://www.cysec.gov.cy/en-GB/entities/investment-firms/cypriot/

Although CySEC is the most prevalent regulator in the EEA, all other European regulators, such as the Finansinspektionen (FI) of Sweden and the Bundesbank and the Federal Financial Supervisory Authority (BaFin) of Germany, are also required to follow the MiFID legislation and are also considered excellent regulators.

Very few Forex brokers operate in the United States. Only brokers regulated by the Commodity Futures Trading Commission (CFTC) can carry out services in the US. All CFTC-regulated Forex brokers must also be members of the National Futures Association (NFA), a self-regulatory organisation. The CFTC has very strict regulatory requirements, which protect traders, but limits their trading freedoms.

Regulatory Rules:

There are many other less strict regulators around the world, and Forex brokers will hold licences with them to avoid the restrictions placed on them by ASIC, CySEC and the FCA. These regulators are often based in small island states and are known as “offshore” regulators.

Common offshore regulators include the Seychelles FSA, the Mauritius FSC, the St Vincent and Grenadines FSA, the Belize IFSC and the Bahamas SCB. While being regulated by one of these smaller regulators does not mean that a broker is bad, it does mean that traders are not as well protected.

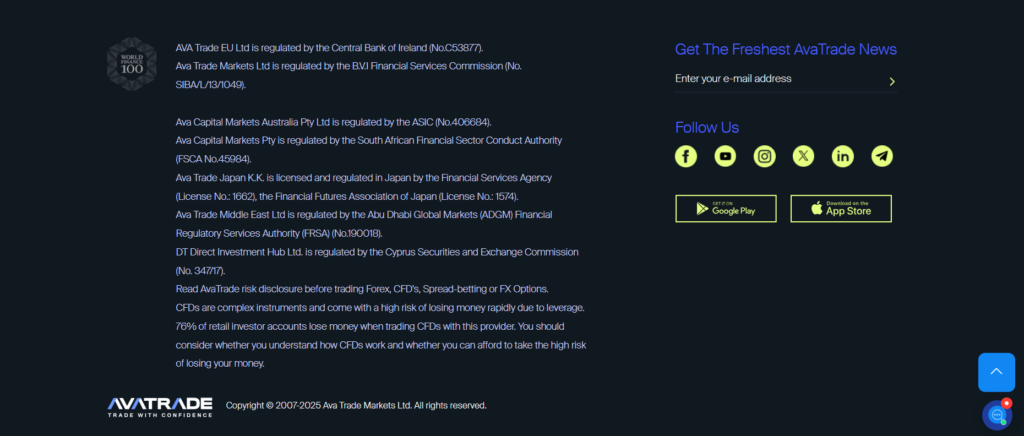

The best and most trustworthy brokers are regulated by at least one of the three major regulators (FCA, CySEC, ASIC) or the FSCA. It is common for brokers to have multiple regulators, one for each region in which they operate. A good example of this is Avatrade. Below is a screenshot from the bottom of their website:

We can see that ASIC, CySEC, the FSCA, Financial Services Agency of Japan, FRSA, and B.V.I regulate AvaTrade and its subsidiary companies. Traders will, therefore, register an account with the relevant subsidiary based on their country of residence. For example, traders in South Africa will be onboarded through the subsidiary regulated by the FSCA, while Australian residents will be onboarded through the ASIC-regulated entity.

If you have been the victim of a scam, you should always contact your local regulator to make a complaint. Although they may not be able to retrieve your money, financial regulators will become aware of these brokers and can take action against them.

We also collect information on scam brokers. Please inform us of any fraudulent activity you have encountered by filling out the scam broker report. To validate the trustworthiness of a broker, use our broker trust checker.

Watch our video on how to spot a scam broker:

Explore more resources that fellow traders find helpful! Check out these other guides to enhance your forex trading knowledge and skills. Whether you’re searching for the best brokers, educational material, or something more specific, we’ve got you covered:

Discover how Forex Trading works with our essential guide. Understand key terminology with examples and learn how to make your first successful trade.

We’ve tested hundreds of Forex brokers to find the safest, low-cost, and reliable brokers. Compare fees, and features—trade smarter with expert insights!

Explore the best Forex brokers for beginners, with user-friendly platforms, educational resources, and demo accounts.

Partner Manager and Financial Writer

Head of Content

Financial Writer