Page Navigation

Select a different country or region to view content tailored to your location.

Alison Heyerdahl is the Head of Content at FxScouts, a Chartered Market Technician (CMT), and an experienced trader, as well as a financial writer with extensive expertise in Forex trading, broker analysis, and market research. She has reviewed 100+ brokers, publishes weekly YouTube trading videos, and co-hosts the “Let’s Talk Forex” podcast.

Click here to download the full report

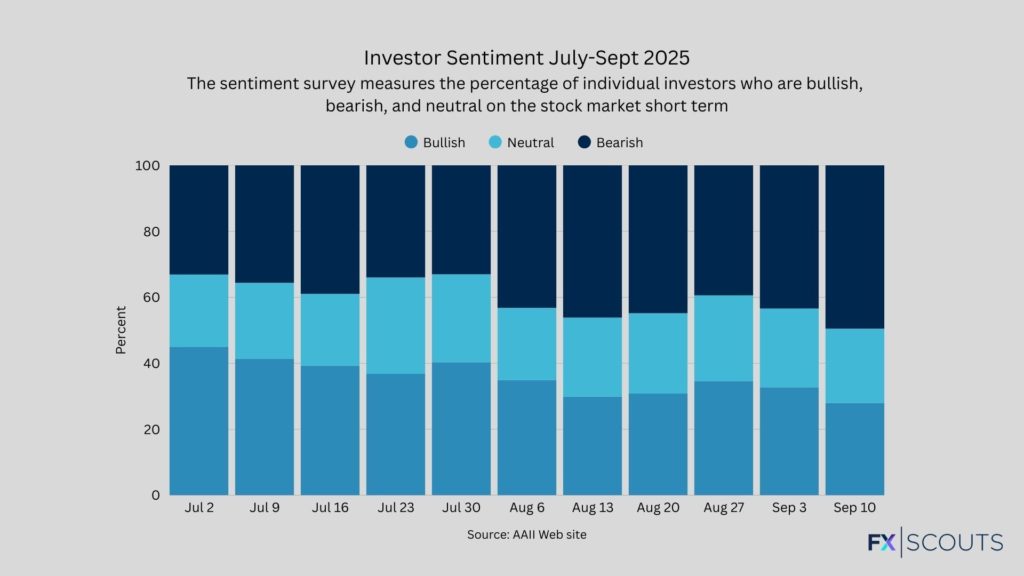

The third quarter of 2025 was dominated by the U.S. dollar’s swings and an accelerating collapse in investor confidence.

Although the dollar’s volatility dominated headlines, the broader foreign exchange market told a story of divergence. The euro, badly hit in July by tariff disputes, regained ground in August and September as the Federal Reserve’s dovish tilt became the prevailing narrative. Sterling followed a similar path, benefiting from relative policy stability in the UK. The yen enjoyed safe-haven demand through much of the quarter, strengthening significantly against the dollar during August and September. Commodity currencies were the standout performers, rising sharply on the back of both higher commodity prices and the weakening dollar.

Central bank dynamics reinforced these moves. While the Fed became trapped by political pressure and deteriorating data, the ECB and Bank of England continued cautiously along the path of gradual policy normalization. The Bank of Japan, though less active than earlier in the year, was perceived as a more credible institution in contrast to the politicised Fed.

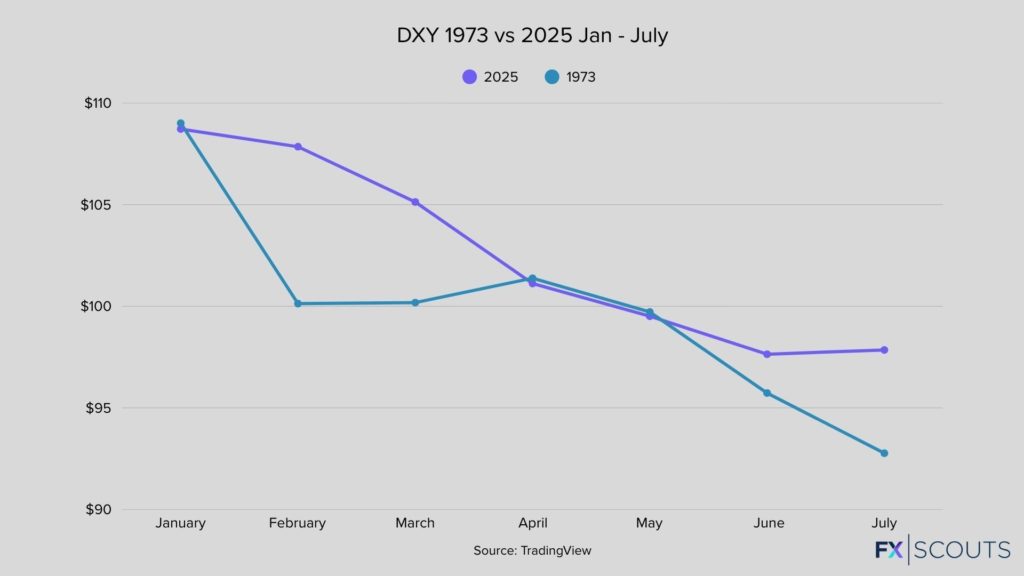

After suffering its steepest first-half decline since 1973, the greenback staged a remarkable rebound in July.

The dollar index (DXY) gained 3.2 percent — its best month in three years — as Trump’s tax cut bill passed and tariff threats of 30 percent or more reignited haven demand. The rally culminated in the U.S.–EU tariff agreement on July 28, which sent EUR/USD down three percent in just three trading days.

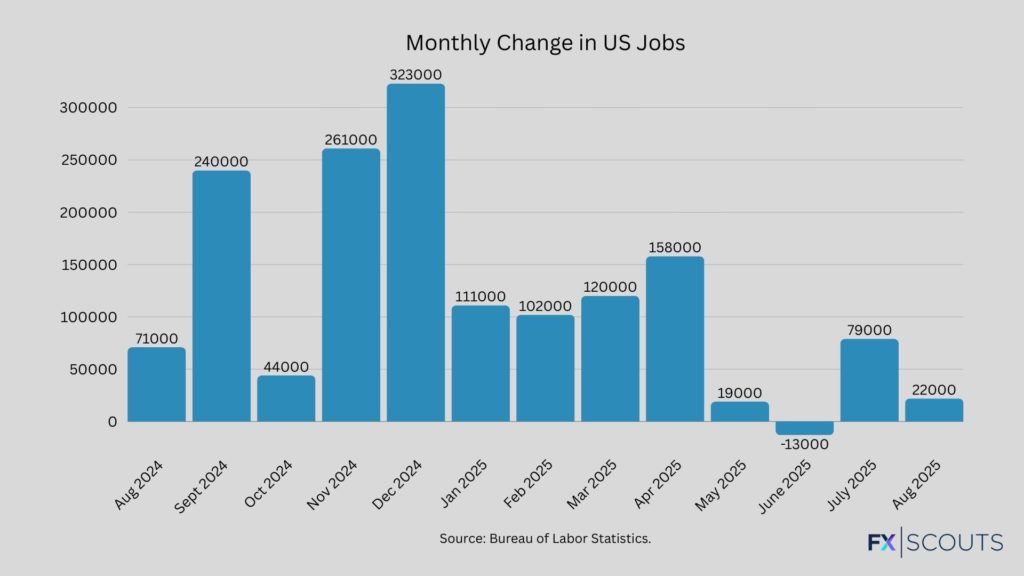

That brief resurgence gave way to crisis in August. The August 1 NFP came in much weaker than expected, while May and June were revised sharply lower. Markets, caught off guard after upbeat earnings and a strong ADP report, immediately priced in a September Fed cut. The dollar fell against all major currencies, with the USD/JPY dropping more than two percent in a single session.

Investor confidence worsened when President Trump dismissed the Bureau of Labor Statistics commissioner, accusing her of fabricating data to make the Republicans and Trump “look bad”. Trump’s attempt to remove Fed Governor Lisa Cook at the end of August underscored fears over institutional independence, deepening investor concern.

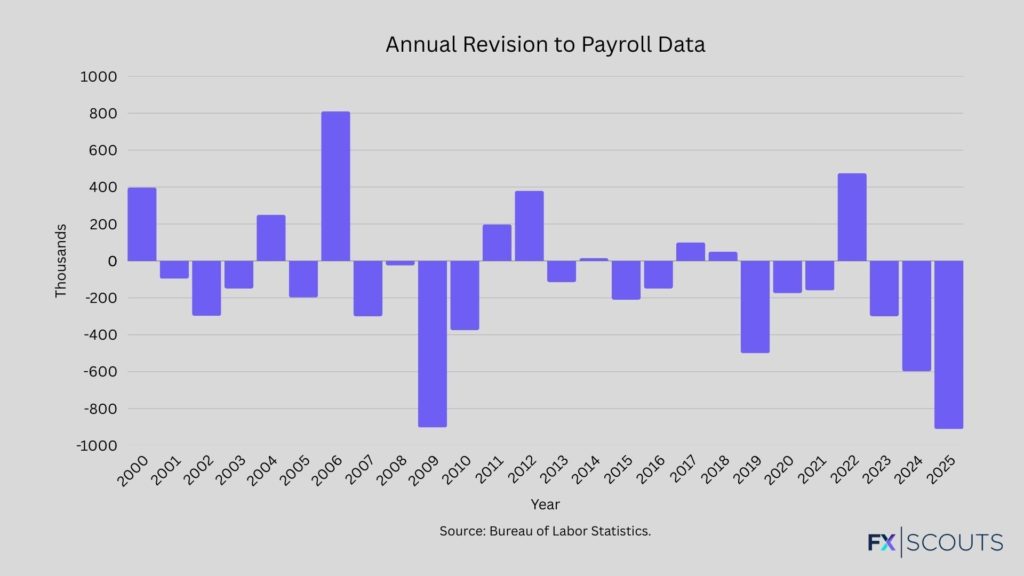

September sealed the quarter’s tone. The September 5 NFP showed just 22,000 new jobs against expectations of 75,000, while unemployment rose to 4.3 percent. Four days later, the BLS announced a downward revision of 911,000 jobs, the largest in its history.

Traders assigned a 96 percent probability to a Fed rate cut, and the dollar came under sustained pressure. Commodity currencies surged: the Australian and Canadian dollars gained as investors chased higher commodity prices, while the South African rand rallied on renewed inflows. Gold, meanwhile, hit a series of all-time highs as investors sought a haven from dollarized assets. The Fed’s 0.25 percent rate cut on September 17, paired with guidance for two more cuts this year despite inflation projected around 3 percent, only reinforced that rotation. The message was clear: monetary policy was tilting decisively toward growth support, and higher inflation was secondary.

The themes of the quarter are clear. Q3 was not about relative growth or interest rate differentials, but about trust. The dollar’s credibility eroded with every data shock and political intervention, and global capital responded by seeking alternatives. What began as a technical rebound in July ended in September with the greenback under siege — and other currencies reaping the benefits.

Explore more resources that fellow traders find helpful! Check out these other guides to enhance your forex trading knowledge and skills. Whether you’re searching for the best brokers, educational material, or something more specific, we’ve got you covered:

Discover how Forex Trading works with our essential guide. Understand key terminology with examples and learn how to make your first successful trade.

We’ve tested hundreds of Forex brokers to find the safest, low-cost, and reliable brokers. Compare fees, and features—trade smarter with expert insights!

Explore the best Forex brokers for beginners, with user-friendly platforms, educational resources, and demo accounts.

Partner Manager and Financial Writer

Head of Content

Financial Writer