Page Navigation

Select a different country or region to view content tailored to your location.

Alison Heyerdahl is the Head of Content at FxScouts, a Chartered Market Technician (CMT), and an experienced trader, as well as a financial writer with extensive expertise in Forex trading, broker analysis, and market research. She has reviewed 100+ brokers, publishes weekly YouTube trading videos, and co-hosts the “Let’s Talk Forex” podcast.

Click here to download the full report

The first quarter of 2026 was defined by a clear shift in narrative, as markets moved through two distinct phases. The early part of the quarter extended trends that had emerged in late 2025, with investors rotating away from US assets amid concerns over valuations, policy credibility, and relative opportunities abroad. This was reflected in a weaker US dollar, a stronger euro, and continued diversification of capital into non-US markets. However, this structural reallocation was abruptly interrupted in mid-February by escalating tensions in Iran—culminating in the joint US/Israeli attack on February 28—which triggered a sharp rise in oil prices and introduced a new inflationary shock into the global economy.

This development fundamentally altered the macroeconomic backdrop. With inflationary pressures re-emerging through energy markets, central banks—particularly the Federal Reserve—faced a renewed policy dilemma. Having only recently begun adjusting policy, policymakers were forced to reassess their trajectory amid rising input costs, persistent uncertainty, and limited visibility into underlying economic conditions.

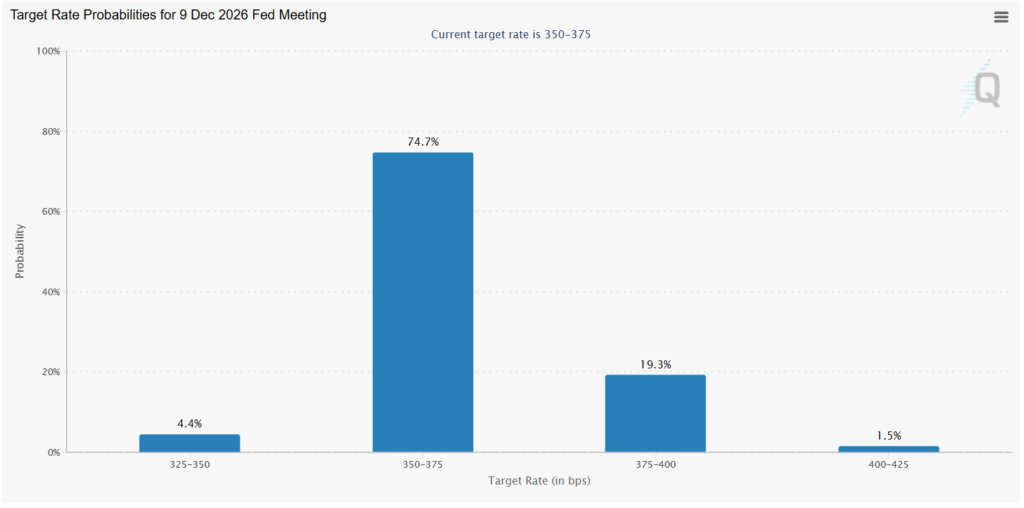

CME FedWatch, which tracks expectations for the Fed’s rate decisions, now shows no chance for rate cut this year with the 20% chance of a rate hike by December.

At the same time, recent FOMC projections highlight a deeply divided committee, with policymakers split between no cuts, one cut, and multiple cuts over the coming year. This divergence underscores the uncertainty facing markets. The approaching arrival of Kevin Warsh as Chairman of the Fed has added a further layer of uncertainty around the future direction of US monetary policy, reinforcing concerns around credibility and consistency first observed in Q4.

Financial markets responded in a manner that highlighted the shift between these two regimes. In the early part of the quarter, US equity markets remained resilient despite elevated valuations, supported by continued positioning and expectations of policy easing. However, following the escalation in geopolitical tensions, this resilience began to fade. The surge in oil prices and renewed inflation concerns pushed back expectations for monetary easing, tightening financial conditions at a time when positioning remained heavily skewed toward equities. As a result, volatility increasingly translated into directional weakness, with sell-offs no longer fully retraced. While broad capitulation has yet to emerge, price action suggests that underlying fragility is becoming more visible. Since the start of the war, the S&P 500 is down around 9% while both the FTSE 100 and the EURO STOXX 50 have both fallen by over 10%.

In currency markets, the US dollar’s behaviour reflected this transition. During the first phase of the quarter, the dollar remained under pressure as capital flowed away from US assets. However, this dynamic reversed following the onset of the Iran conflict, with the DXY strengthening as investors sought safety amid rising geopolitical risk, higher oil prices, and shifting rate expectations. As a net energy exporter, the United States benefits from higher oil prices, while rising inflation expectations pushed rate cuts further out. However, this shift appears to be driven by the current shock, rather than a broader restoration of confidence in US assets.

The euro, by contrast, came under renewed pressure in the latter part of the quarter, reflecting the Eurozone’s greater vulnerability to rising energy prices. As a net energy importer, the region faces a more direct inflationary impact from higher oil costs, increasing downside risks to growth and complicating the European Central Bank’s policy outlook. This marked a clear reversal from the early part of the quarter, when EUR/USD had strengthened amid capital outflows from US assets, highlighting the extent to which the geopolitical shock altered prevailing market dynamics.

Elsewhere, Japanese 10Y bond yields hit their highest level since 1999, and the USD/JPY continues to hover just below 160, a traditional threshold for BOJ intervention. Japan imports 95% of its oil from the Middle East, meaning the country must convert yen into dollars to pay for energy. With oil prices spiking, the BOJ finds itself in an increasingly uncomfortable position.

Rate hikes would strengthen the yen and ease import cost pressures, but they would also slow an economy already absorbing an energy shock it did not choose. With the new Prime Minister, Sanae Takaichi, already pursuing record fiscal stimulus, inflationary pressure is intensifying. The BOJ kept rates stable in their meeting on 19 March, but many analysts predict an increase in the April or June meetings. While the yen carry trade remains stable currently, any serious intervention to defend the yen or a widespread escalation in the conflict could lead to a sharp unwinding.

Gold initially extended its strong rally into early Q1 but faced a significant correction at the end of January as speculators engaged in profit-taking following the nomination of Kevin Warsh as Chairman of the Fed. While prices stabilized thereafter, the war in Iran forced a sharp reversal as rising yields, a stronger US dollar, and shifting rate expectations reduced the appeal of non-yielding assets. This divergence highlights the increasingly complex nature of traditional safe havens, with gold caught between inflationary pressures that would typically support prices and tighter financial conditions that act as a constraint. Meanwhile, crypto markets continued to behave as high-beta risk assets, with Bitcoin falling as low as 62k in February before recovering to end the quarter near the 70k mark.

Taken together, Q1 2026 was not defined by a single narrative, but by the interaction between a structural rotation away from US assets and a geopolitical shock that has sown chaos into the markets. This shift has left traders navigating a more complex and conditional regime, in which asset behaviour is shaped not only by underlying fundamentals, but by the nature and origin of the shocks driving them.

Explore more resources that fellow traders find helpful! Check out these other guides to enhance your forex trading knowledge and skills. Whether you’re searching for the best brokers, educational material, or something more specific, we’ve got you covered:

Discover how Forex Trading works with our essential guide. Understand key terminology with examples and learn how to make your first successful trade.

We’ve tested hundreds of Forex brokers to find the safest, low-cost, and reliable brokers. Compare fees, and features—trade smarter with expert insights!

Explore the best Forex brokers for beginners, with user-friendly platforms, educational resources, and demo accounts.

Partner Manager and Financial Writer

Head of Content

Financial Writer